Randomness

The elements introduced so far (clocks, events and processes) let us describe event sequences in discrete event systems (DES). In reality those sequences often show considerable randomness and come out starkly different with varying initial conditions or intervening random events.

Random initial states, transition probabilities or stochastic event times can be computed by using a Distribution.

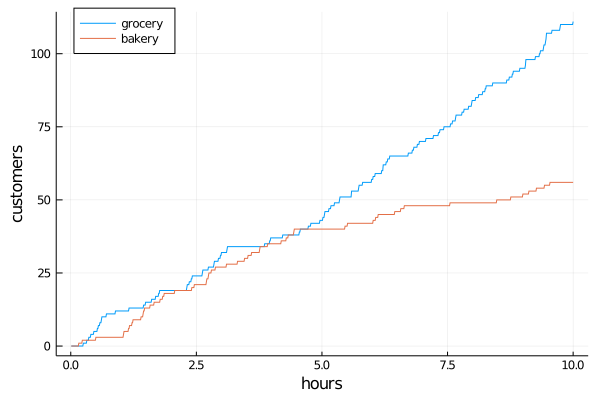

Two Poisson Processes

In the following example we simulate two arrival processes, one homogeneous poisson process (HPP) say for a grocery store and one non-homogeneous poisson process (NHPP) where the number of arrivals diminish over time e.g. for a bakery.

using DiscreteEvents, Random, Distributions, Plots

Random.seed!(1234) # set random number seed for reproducibility

const λ = 10 # arrival rate 10 customers per hour

const ρ = log(0.2)/10 # decay rate for customer arrivals

D = Exponential(1/λ) # interarrival time distribution

hpp = [0] # counting homogeneous arrivals

nhpp = [0] # counting non-homogeneous arrivals

t = Float64[] # tracing variables

y1 = Int[]

y2 = Int[]

δ(t) = Int(rand() ≤ exp(ρ*t)) # model time dependent decay of arrivals

trace(c) = (push!(t, c.time); push!(y1, hpp[1]); push!(y2, nhpp[1]))

# define two arrival functions

arr1() = hpp[1] += 1

arr2(c) = nhpp[1]+= δ(c.time)

# create clock, schedule events and tracing and run

c = Clock()

event!(c, arr1, every, D) # HPP arrivals (grocery store)

event!(c, fun(arr2, c), every, D) # NHPP (bakery)

periodic!(c, fun(trace, c))

run!(c, 10)

plot(t, y1, label="grocery", xlabel="hours", ylabel="customers", legend=:topleft)

plot!(t, y2, label="bakery")

δ(t) defines a time dependent probability of a state transition (customer arrival). Using the distribution D in event! creates stochastic time sequences $(t_1, t_2, t_3, ...)$ of poisson processes.